Credit Portfolio Management (CPM) is evolving from a static risk-monitoring function into a strategic driver of capital efficiency and enterprise resilience. The blog explores key shifts—rising borrower complexity, regulatory changes, AI-led analytics, and integrated treasury alignment. It outlines modern CPM pillars like dynamic risk appetite, scenario stress testing, sectoral rebalancing, and operating model transformation—urging banks to embrace data-driven, proactive approaches to navigate volatility and meet stakeholder expectations.

Credit Portfolio Management (CPM) is no longer a back-office, risk-monitoring exercise—it has evolved into a strategic function that shapes how banks navigate uncertainty, optimize capital, and deliver sustainable value to stakeholders. As financial institutions face a complex blend of economic cyclicality, regulatory evolution, sectoral risk concentrations, and digital disruption, CPM leaders are reimagining their roles from passive risk aggregators to proactive value creators.

This shift demands a reconfiguration of traditional frameworks. Institutions that embed forward-looking analytics, dynamic risk appetite alignment, and collaborative liquidity strategies into their CPM approach will be better equipped to manage volatility, preserve portfolio health, and support enterprise growth.

Why CPM Must Evolve Now

The global credit risk assessment market is projected to grow from $9.55 billion in 2025 to $31.46 billion by 2034—a CAGR of 14.2%. This rapid growth signals a fundamental shift in how financial institutions assess, manage, and mitigate credit risk. Beyond market expansion, there are several structural forces that are reshaping how banks must approach credit portfolio management.

- Rising borrower complexity and sectoral interdependence: The nature of credit exposure is becoming more interconnected across supply chains, sectors, and geographies. Institutions must capture this complexity in risk modeling and exposure mapping.

- Changing regulatory and capital frameworks: Global moves toward Basel IV (or Basel III endgame), climate-related financial disclosures, and enhanced risk-weighted asset calculations require continuous recalibration of credit portfolios.

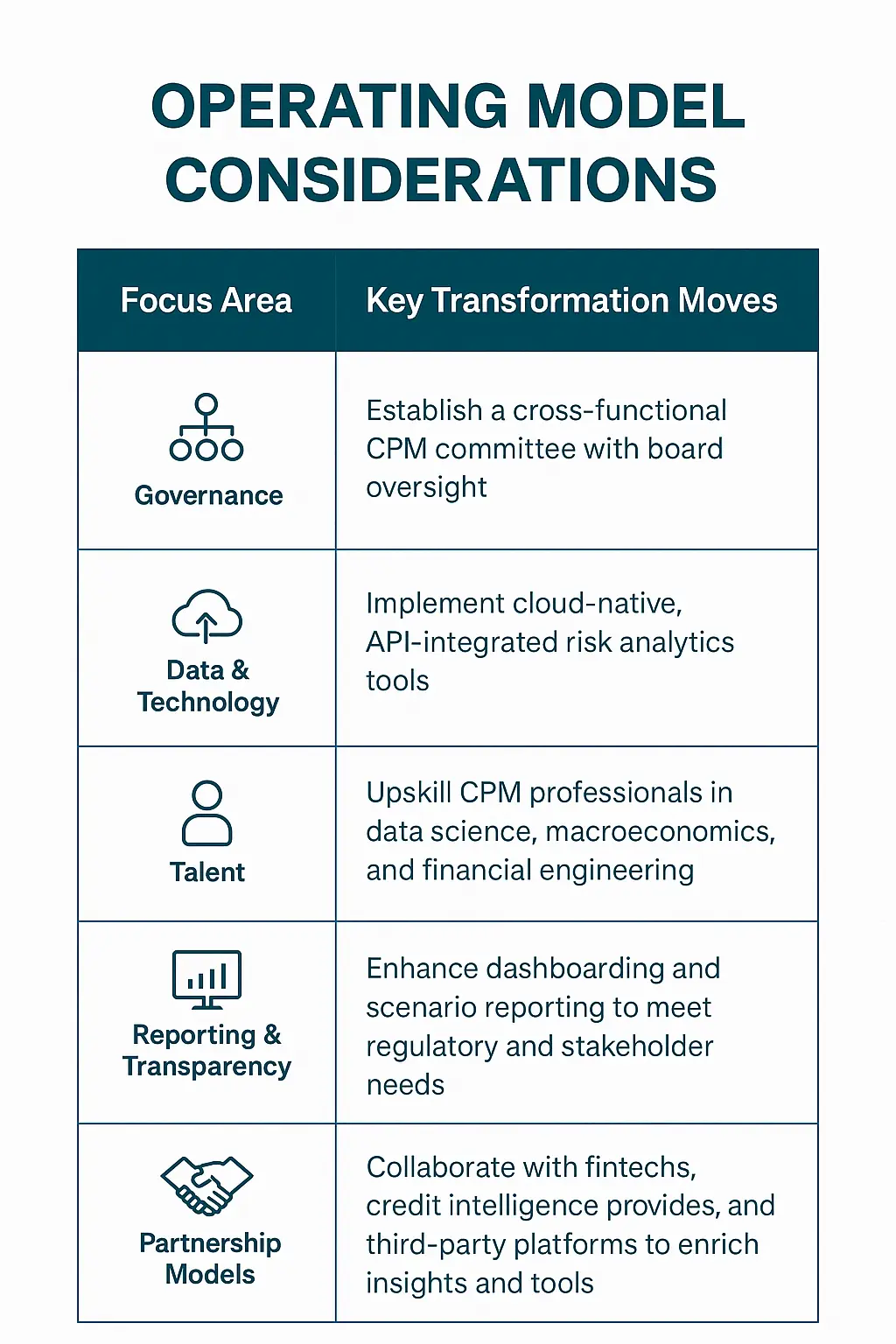

- Technology and data modernization: Banks that leverage real-time data streams, AI-driven risk analytics, and digital borrower segmentation are outperforming peers still reliant on static risk models.

- Stakeholder expectations for transparency and governance: Investors, regulators, and boards demand greater clarity on how institutions are stress testing, rebalancing, and capitalizing their credit books in response to external and internal pressures.

JPMorgan has allocated $18 billion to technology, integrating over 175 AI tools, and reported $1.5 billion in cost savings from AI-driven fraud prevention, personalization, and credit processes.

Strategic Pillars for Next-Generation Credit Portfolio Management

- Dynamic Risk Appetite Alignment

CPM must work in sync with Enterprise Risk and Business Strategy to continuously adjust exposure thresholds across credit types, industries, and geographies. Leading institutions establish real-time feedback loops between portfolio health indicators and origination pipelines to control risk accumulation.

- Scenario-Based Portfolio Stress Testing

Rather than relying on fixed annual stress tests, forward-looking banks employ scenario libraries covering macroeconomic downturns, geopolitical shocks, climate risk events, and digital disruption. These tests feed directly into capital planning, provisioning strategies, and credit reallocation decisions.

- Sectoral Diversification and Thematic Rebalancing

To mitigate concentration risks, CPM teams actively shift exposures toward more resilient or emerging sectors, such as:

- Infrastructure and clean energy (green finance)

- Healthcare and senior living

- Technology-driven SMEs

- Export-linked and resilient manufacturing hubs

This requires both internal expertise and access to market-based instruments (loan syndications, credit default swaps, securitizations) for portfolio reconfiguration.

- Integration with Treasury, Capital, and Liquidity Management

Modern CPM is integrated with ALM, Treasury, and Finance to ensure alignment of:

- Duration profiles and cash flow predictability

- Capital optimization through RWA efficiency

- Liquidity buffers under multiple drawdown and market stress scenarios

This cross-functional orchestration supports regulatory compliance and strengthens institutional resilience.

- AI and Data-Driven Early Warning Systems

89% of finance teams still use Excel—but adoption of AI/ML for predictive modeling is growing However, by deploying machine learning models and digital intelligence platforms, financial institutions can detect early signs of –

- Borrower stress signals

- Sector-specific deterioration trends

- Emerging systemic threats

Advanced institutions integrate these insights directly into underwriting, pricing, and portfolio rebalancing engines, enabling real-time risk mitigation.

Conclusion

Credit Portfolio Management is entering a new era—one where strategic foresight, integrated intelligence, and proactive intervention define success. In this environment, banks and financial institutions must adopt agile, data-driven, and enterprise-aligned CPM models to remain competitive, compliant, and resilient.

At Anaptyss, we partner with forward-looking institutions to modernize credit portfolio practices through advanced analytics, digital transformation frameworks, and regulatory-aligned operating models—driving risk-adjusted performance and long-term portfolio sustainability.

For a conversation on how we can support your CPM modernization journey, contact us at info@anaptyss.com.