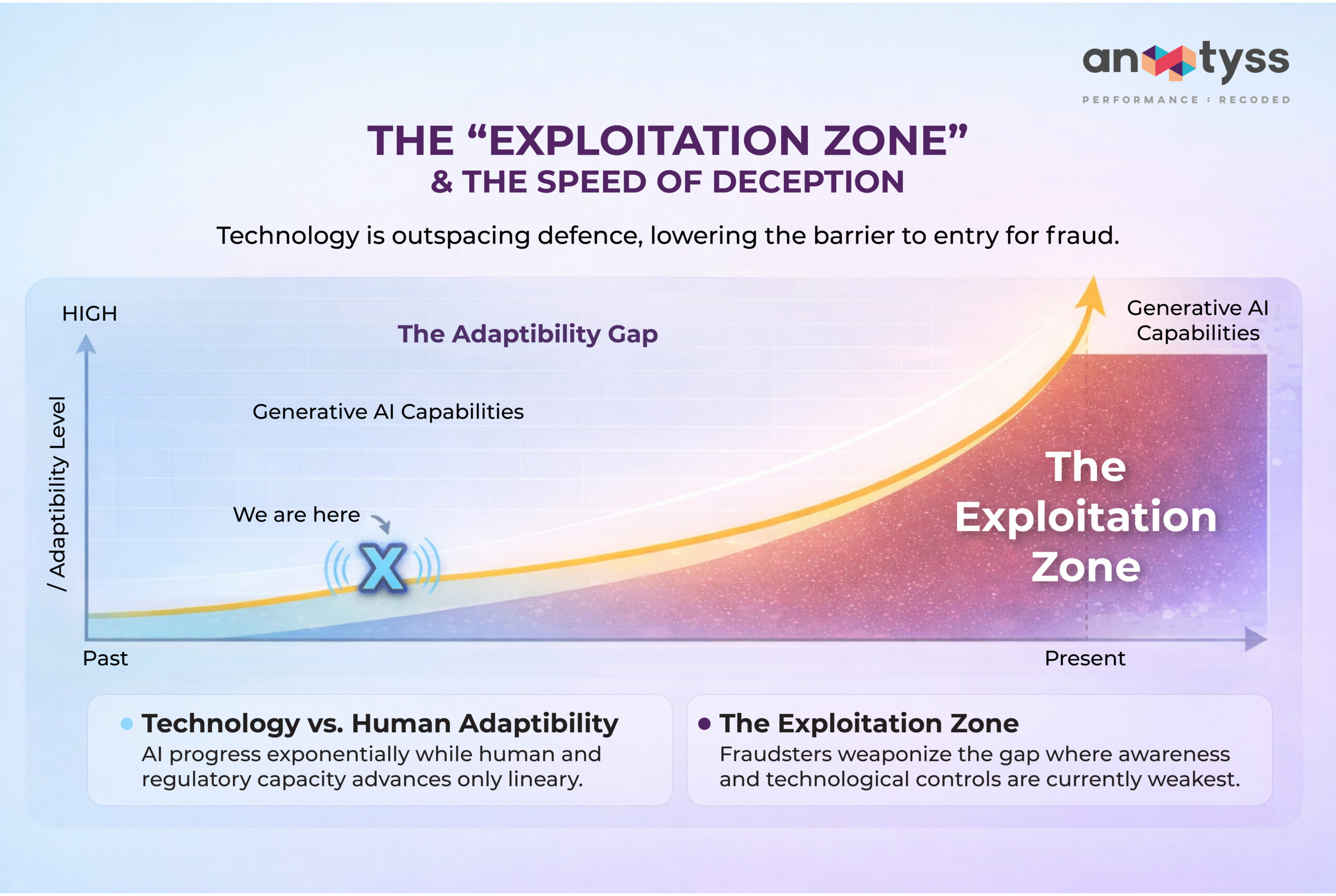

For decades, the financial services industry relied on the premise that biometric markers—fingerprints, facial geometry, and vocal characteristics—were immutable and unforgeable. That assumption has collapsed. We are currently navigating what security strategists term the “Exploitation Zone”—a widening chasm between the exponential advancement of generative AI and the linear adaptation of institutional defense mechanisms.

The threat is no longer theoretical. For instance, in early 2024, a finance professional at a multinational firm was deceived into wiring $25.6 million to fraudsters. The employee was not tricked by a simple phishing email, he was manipulated during a live video conference where the company’s CFO and several colleagues appeared and spoke. They were all deepfakes, generated using public audio and video footage.

This incident, alongside the earlier $35 million heist involving a cloned voice of a company director in the UAE, signals a paradigm shift. For financial institutions, sensory evidence like seeing a face or hearing a known voice can no longer be considered sufficient proof of identity.

The Democratization of Deception

Historically, high-fidelity voice cloning required Hollywood-level budgets and hours of studio-quality audio. Today, the barrier to entry has vanished. Generative AI tools, some available for free or as little as $5 a month, can clone a voice with startling accuracy using as little as three seconds of audio,. This audio can be scraped from a LinkedIn video, a recorded webinar, or a voicemail greeting.

Modern synthesis architectures, such as flow-matching and hierarchical neural codecs, have moved beyond the robotic, disjointed speech of early text-to-speech systems. Today’s AI models, including Dia2 and Maya1, incorporate streaming context awareness and emotional expression. They can replicate the cadence, intonation, and even the “micro-pauses” of human speech, effectively bypassing the human ear’s ability to detect fraud. Studies indicate that human listeners perceive AI-generated voices as “real” approximately 80% of the time.

Consequently, the attack surface for banks has expanded dramatically. Fraud attempts in the financial services sector rose by 21% between 2024 and 2025, with one in every twenty verification attempts now identified as fraudulent.

The Failure of Legacy Biometrics

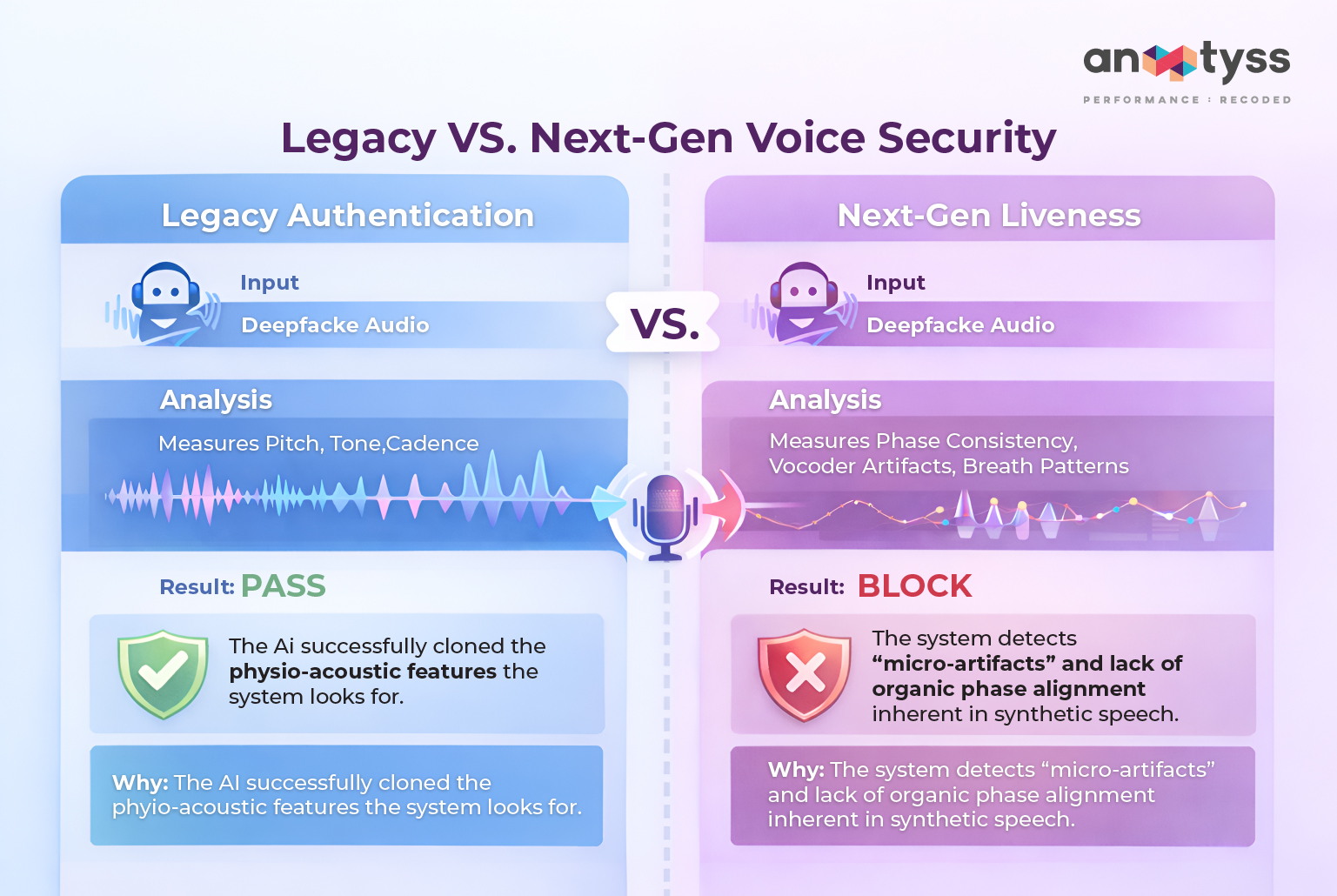

For years, financial institutions have promoted voice authentication as a secure, frictionless alternative to passwords. Customers were told, “My voice is my password.” However, legacy voice biometric systems primarily analyze physical characteristics—pitch, tone, and the spectral envelope of the vocal tract.

The vulnerability lies in the fact that generative AI creates a digital twin that possesses these exact mathematical characteristics. If a security system is designed to ask, “Does this sound like the customer?”, an AI clone will result in a positive match. The system fails because it is asking the wrong question. In an era of generative AI, the critical question is no longer “Who is speaking?” but “Is a human speaking?”.

Without robust “liveness detection,” voiceprints are susceptible to replay attacks and real-time voice conversion, where a fraudster speaks into a microphone and the software instantly translates their words into the victim’s voice.

The Regulatory Mandate is to Move Beyond Single-Factor

The regulatory environment in the United States is rapidly pivoting to address these vulnerabilities. The Federal Financial Institutions Examination Council (FFIEC) issued guidance in 2021 explicitly stating that single-factor authentication is inadequate for high-risk transactions. Relying solely on a voiceprint (an “inherence” factor) creates a single point of failure.

The FFIEC advises that financial institutions must implement layered security and multi-factor authentication (MFA) for users accessing high-risk systems or moving funds. This aligns with broader cybersecurity frameworks which emphasize that if one gate is breached (e.g., a voice clone tricks the IVR), subsequent gates must remain locked.

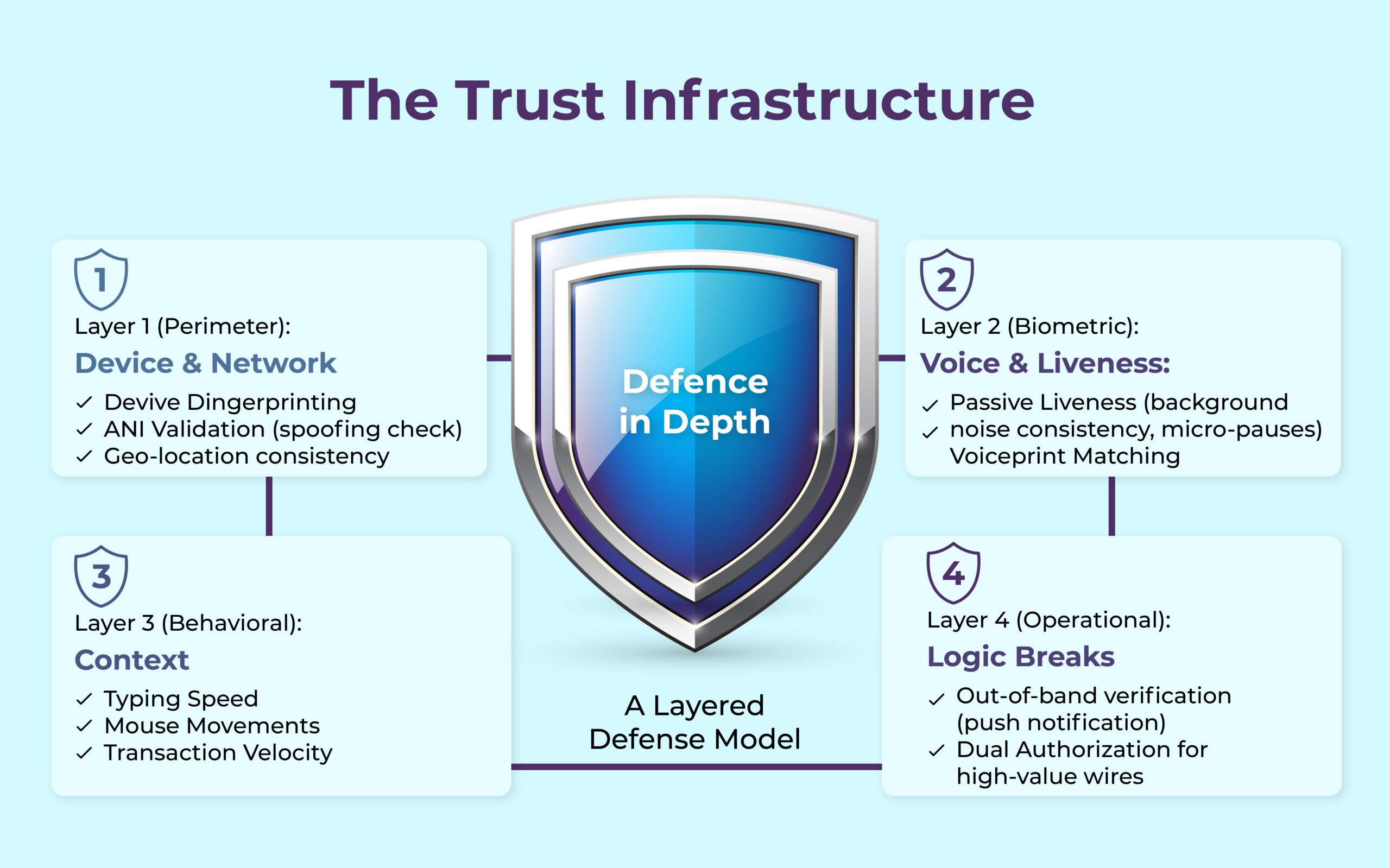

Strategic Defense – A Layered Architecture

To mitigate the risk of deepfake fraud, financial leaders must transition from simple verification to a comprehensive “Trust Infrastructure”. This requires a defense-in-depth strategy comprising three pillars: Technology, Context, and Operations.

1. Technological Defense: Liveness Detection

Voice biometrics must be upgraded to include liveness detection. This technology analyzes the audio signal for artifacts that human ears miss—such as synthetic phase inconsistencies, the absence of organic breath patterns, or the specific digital signatures left by neural vocoders,.

- Active Liveness requires the user to repeat a randomized phrase (challenge-response). While secure, it adds friction.

- Passive Liveness analyzes the voice in the background during natural conversation. This is increasingly the industry standard for contact centers, as it balances security with customer experience.

2. Contextual Defense: Behavioral and Device Signals

Identity must be triangulated. Even if the voice is a perfect match, the surrounding context provides the “tell.”

- Device Fingerprinting is the call originating from a recognized device? Has the device been associated with previous fraud?.

- Behavioral Biometrics to understand how does the user interact with the application? Are they typing at a superhuman speed? In a voice context, are they using a VoIP line associated with a known botnet?

- ANI Validation for Automatic Number Identification matching. This ensures the call isn’t being spoofed from a different location.

3. Operational Defense: Process Breaks

For high-value interactions—such as wire transfers or changing authorized users—technology should be the floor, not the ceiling.

- Out-of-Band Verification – If a request comes via voice or video, verify it via a separate channel (e.g., an encrypted message or a push notification to a trusted device).

- Dual Authorization – Require approval from two separate authorized personnel for transfers exceeding a certain threshold.

- Eliminate “Executive Override” – Fraudsters rely on the authority bias. Protocols must strictly prohibit bypassing security checks, regardless of who is purportedly on the line.

Conclusion

The “Exploitation Zone” will persist as long as technology outpaces adaptation. However, financial institutions are not helpless. By treating deepfakes not as a technological novelty but as a systemic risk management challenge, banks can harden their defenses.

The era of trusting sensory evidence is over. The future of banking security relies on “Zero Trust” principles applied to identity: verify every signal, assume breach, and validate liveness. By integrating real-time deepfake detection with robust MFA and strict operational governance, financial institutions can protect their assets and their reputation in an age where seeing and hearing is no longer believing.

To explore how Anaptyss helps financial institutions strengthen fraud defenses, modernize identity verification, and implement layered risk controls across channels, connect with our specialists at info@anaptyss.com.