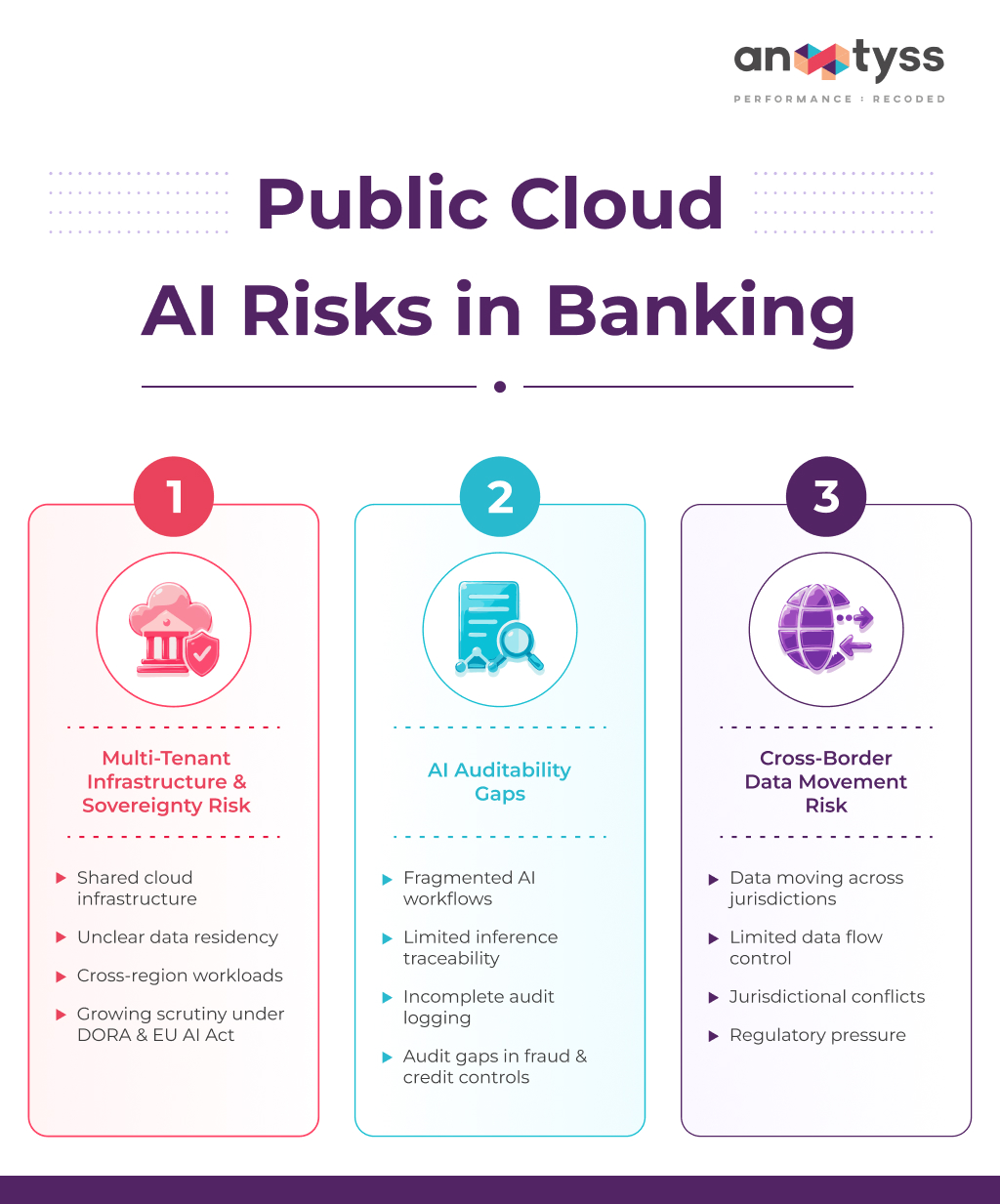

AI in banking now depends on more than model quality; it depends on clear control over where data lives and how it moves. Regulators are focused on whether banks can show and trace data within the right jurisdiction when needed, especially during audits. Because of this, data residency has become a key requirement before AI can be deployed in production.

The banking industry is navigating a high-stakes tension. On one side sits the undeniable pressure to integrate generative and agentic AI for everything from fraud detection to customer engagement. On the other is an increasingly aggressive global regulatory landscape that views data as a matter of national security.

As financial institutions move beyond pilot programs into production-scale AI, data residency—the physical and legal location of data—is no longer a “check-the-box” compliance formality. It has become the foundational control that determines whether an AI strategy can be approved, deployed at scale, or faces costly regulatory intervention.

Why Data Residency Is Becoming a Strategic Banking Control

Data residency is now a core control requirement in US banking AI programs, as AI moves into production use across fraud, credit, and compliance workflows. Regulators and auditors are increasingly focused on whether banks can prove where data is processed, how it moves across cloud environments, and whether those flows are fully traceable in hindsight. With rising reliance on hyperscale cloud platforms and jurisdictional exposure under frameworks like the CLOUD Act, data location has become a direct factor in audit defensibility. As a result, CROs are treating data residency as a precondition for approving production AI systems, not an infrastructure detail.

The Sovereignty Crisis in Global Banking AI

As banks scale AI across borders, they are running into a structural issue: data is governed differently depending on where it is stored, processed, and accessed. This creates a sovereignty challenge that goes beyond infrastructure design and directly impacts regulatory exposure and audit outcomes.

Data Residency vs Data Sovereignty

The distinction between residency and sovereignty is now central to how banks evaluate AI risk.

| Concept | Definition | Control Focus | Banking Implication |

| Data Residency | Where data is physically stored or processed | Infrastructure location | Determines hosting and deployment choices |

| Data Sovereignty | Which legal jurisdiction governs the data | Legal + regulatory authority | Determines compliance exposure and access rights |

The CLOUD Act, GDPR, and Cross-Border Risk

Cross-border data laws are creating overlapping and sometimes conflicting obligations for global banks.

| Regulation | Primary Jurisdiction | Key Control Impact |

| CLOUD Act | United States | Enables lawful access to data held by US-based providers, regardless of storage location |

| GDPR | European Union | Restricts processing and transfer of personal data outside approved jurisdictions |

| Emerging AI regulations (EU AI Act) | EU | Adds requirements for explainability, traceability, and data governance in AI systems |

Digital sovereignty is becoming a control requirement, not a geopolitical concept. For banking AI programs, this means that architectural decisions about where models run, where data is stored, and how inference results are logged are now regulatory considerations, not just engineering choices.

In practice, it directly determines whether AI systems can be approved, audited, and scaled across regions without regulatory friction.

How Global AI Regulations Are Reshaping Banking Controls

AI regulation is becoming increasingly fragmented by jurisdiction, forcing banks to design control frameworks around regional requirements rather than global standards.

The Brussels Effect and the EU AI Act

The EU is setting global expectations through its risk-based AI regulation, often referred to as the “Brussels Effect.” The EU AI Act requires high-risk AI systems—such as credit scoring and fraud detection—to be explainable, auditable, and transparent. This effectively raises the baseline for AI governance, even for banks operating outside the EU but serving global markets.

DORA and Cloud Concentration Risk

The Digital Operational Resilience Act (DORA) shifts focus from system performance to infrastructure dependency. Banks must now manage and demonstrate resilience against cloud concentration risk, making reliance on a single provider or tightly coupled services a regulated control concern.

Data Localization in India and China

India and China enforce strict data localization through regulations like DPDPA and PIPL, requiring certain data to remain within national borders. This limits centralized AI architectures and forces banks to adopt region-specific data and control designs.

Conclusion – From Compliance Burden to Competitive Edge

The future of banking AI will be defined by infrastructure trust. As AI becomes embedded in core risk and compliance workflows, banks need confidence not just in outputs, but in where data is processed and how it is governed.

Data residency sits at the center of this shift, ensuring AI systems operate within defined jurisdictions, align with regulatory expectations, and remain defensible in audits and approvals.

In this environment, control becomes the real differentiator in scaling AI responsibly.

ANA is built to support this model, enabling AI-assisted control testing and assurance within secure, governed enterprise environments where data, model inference, and oversight remain fully within bank-defined boundaries and governance frameworks.

Explore how ANA helps banks scale AI with stronger governance, auditability, and data control at info@anaptyss.com.