In this blog, explore the critical role of Financial Crime Compliance (FCC) in protecting banks and financial institutions from financial crimes like money laundering and fraud. Learn about the challenges of compliance, including rapidly changing regulations and high costs, and discover how digital solutions can enhance your FCC strategies. Understand the importance of adhering to regulatory requirements such as the Bank Secrecy Act (BSA), Know Your Customer (KYC), and OFAC sanctions to mitigate risks and maintain a strong reputation.

Financial Crime Compliance (FCC) is a process to ensure your bank or financial institution is meeting the policies, standards, and regulations laid by the Financial Crimes Enforcement Network (FinCEN) of the United States Treasury Department.

Meeting financial crime compliance is a legal requirement for banks and financial institutions to combat the various financial crime risks and activities. It helps banks and financial institutions detect, prevent, and report illegal financial activities.

The blog discusses the financial crime risks in banking and financial institutions, the cost of financial crimes, and associated challenges. It also highlights the importance of digital solutions to combat financial crimes and strategies to meet the Financial Crime Compliance (FCC) and various other regulatory requirements.

What is Financial Crime?

Financial crime is criminal conduct involving malicious acts against banks and financial institutions committed by individuals, groups, or criminal organizations to steal, manipulate, launder money, finance terrorism, and obtain financial gains and professional advantage.

Financial crime can have devastating impacts on the social and emotional well-being of individuals. For organizations, failure to inculcate financial crime compliance can have significant financial and reputational losses to the organizations. ]

Following are some examples that are normally considered a financial crime,

- Money laundering

- Terrorism financing

- Cybercrime

- Bribery and corruption

- Market manipulation

- Insider dealing

- Tax evasion

- Credit fraud

- Insurance fraud

- Embezzlement

- Theft or forgery

- Slavery/human trafficking

The Importance of Financial Crime Compliance

Financial institutions, such as banks, have always been the prime target for criminals who often exploit the weakness of the sector for personal. Therefore, financial crime compliance has been an important subject that financial institutions cannot ignore.

Financial Crime Compliance helps financial institutions:

1. Protect Against Financial Crimes

FCC serves as a first line of defense protecting financial institutions against financial crimes such as money laundering, fraud, and terrorist financing. With robust FCC policies and internal controls, financial institutions ensure that laws are followed and unethical activities are eliminated to protect themselves as well as their customers.

2. Meet Regulatory Obligations

Financial institutions are subject to a vast array of local and international regulations. Non-compliance can result in severe legal and financial consequences. This includes fines and reputational damage.

In 2021, global financial crime fines totaled $9.95 billion, down from 2020’s record-breaking figure of $22.86 billion. Corruption, bribery, and fraud accounted for 69.6% of FinCrime fines handed out in 2021.

Financial crime compliance (FCC) is not a choice; it’s a responsibility.

3. Preserve Trust and Protect Reputation

A robust FCC program also helps financial institutions bolster their reputation in public space. By adhering to compliance standards, institutions demonstrate their commitment to ethical practices that help maintain trust, drive customers, and ensure business growth. It also helps prevent scandals and adverse media coverage that could damage their reputation.

4. Risk Mitigation

Effective FCC practices reduce the risk of financial loss due to fraud and other financial crimes. Financial crime risk management (FCRM) is a forearm of the FCC that helps ensure that the rules are followed. It involves risk assessments, technology solutions, and workforce training.

Global Financial Crime Compliance Requirements

Adherence to the regulatory requirements is critical for financial crime compliance for banks and financial institutions. They need to prioritize and adhere to the following global requirements for financial crime compliance:

1. Bank Secrecy Act (BSA) and Anti-Money Laundering (AML

Also known as the Currency and Foreign Transactions Reporting Act (CFTRA), the Bank Secrecy Act (BSA) was enacted to identify financial crime activities. Banks and financial institutions are also required to have a robust framework to file reports of cash transactions exceeding $10,000, currency transaction reports (CTRs), and assist the US government to detect and prevent suspected money laundering activities for BSA and anti-money laundering compliance.

2. Know Your Customer (KYC)

Banks and financial institutions are obligated to verify their customer identities (KYC), understand the nature of their business, and assess the criminal risks they pose. The KYC components include,

a. Customer Identification Program (CIP)

CIP is a critical KYC requirement during customer onboarding. This includes collecting customer information, such as full name, date and place of birth, address, and identification number (any document issued by govt authorities, such as passport or SSN for individuals). Banks and financial institutions need to perform the CIP to meet the KYC and customer risk assessment obligations.

b. Customer Due Diligence (CDD)

CDD refers to the set of processes that involves collecting personal information and identifying a customer with solutions, such as documents or biometrics. It also includes the customer risk assessment by checking the customer data against the database for document verification. It is required at the time of opening an account in the bank or financial institution. CDD is required for customers considered to be low-risk.

c. Enhanced Due Diligence (EDD)

EDD involves protocols to verify and assess high-risk customers or individuals by performing additional checks, which may include more documents, additional database verifications, frequent identity verification, or a combination of all of the mentioned checks. Following are some common factors that may trigger the need for EDD of identified high-risk customers or individuals:

- Politically Exposed Person (PEP)

- People linked to financial crime or money laundering activities in the past

- The person is the subject of adverse media

- Individuals on the sanctions list or related to a company or country subjected to sanctions

- A person belonging to a high-risk country.

All FATF members must implement the FATF risk-based approach recommendations to meet CDD and EDD requirements for AML/CFT compliance.

3. OFAC Sanctions Regulations

Office of Foreign Assets Control or OFAC Sanctions compliance program requires banks and financial institutions to implement a robust system in place to prohibit any financial and trade activities with countries, entities, or individuals engaged in state-sponsored criminal activities, breaches of international laws, the proliferation of weapons of mass destruction, and human right violations. Following are the OFAC sanctions types imposed against individuals, entities, and countries.

a. Primary OFAC Sanctions

Targeted against individuals or entities within the US preventing them from trade or commerce activities with US sanctions targets.

b. Secondary OFAC Sanctions

Prohibits the US persons from doing business with third parties residing in foreign countries but not directly subject to the US jurisdiction.

4. The USA PATRIOT Act

The Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism (USA PATRIOT) Act of 2001 puts forth measures “to deter and prosecute financial crime activities, such as money laundering and financing of terrorism.”

By complying with these regulations, banks and financial institutions can prevent and detect financial crimes, such as fraud, money laundering, and financing of terrorism effectively.

5. Sixth EU Anti-Money Laundering Directive (6AMLD) and AMLA (EU)

European Union: The 6AMLD expands predicate offenses to include 22 categories, incorporating cybercrime and environmental crimes for the first time. The directive extends criminal liability to legal persons and increases minimum prison sentences to four years.

6. Beneficial Ownership Transparency

Global beneficial ownership transparency initiatives are accelerating, with countries implementing comprehensive registers to combat illicit finance. However, no country has achieved full transparency as of 2025, indicating significant room for improvement.

The implementation of beneficial ownership reporting requirements continues to evolve, with new AML requirements for Registered Investment Advisors taking effect January 1, 2026.

The push for transparency encompasses:

-

Expanded coverage of all legal vehicles without exceptions

-

Public accessibility requirements for beneficial ownership data

-

Enhanced due diligence for ultimate beneficial owners

-

Approximately 15% of AML/KYC procedures expected to be conducted via blockchain-based systems by 2025

7. FINTRAC

FINTRAC has implemented enhanced compliance requirements with proposed penalties increasing 40-fold, potentially reaching C$20 million for companies and C$4 million for individuals.

8. Crypto Assets & Digital Currencies

Virtual Asset Service Providers (VASPs) are increasingly being brought under stricter regulatory oversight, with requirements such as real-time sanctions screening and adherence to the “travel rule” for information sharing during transactions.

Regulatory frameworks like the European Union’s Markets in Crypto-Assets Regulation (MiCAR) and the OECD’s Global Base Erosion (GloBE) standards are further tightening controls around VASPs to ensure transparency and compliance.

At the same time, Central Bank Digital Currencies (CBDCs) are gaining momentum, with over 100 countries (over 95% of global GDP) actively piloting or implementing CBDC initiatives. These developments are introducing new compliance demands, particularly in areas such as data privacy, cross-border payments, and anti-money laundering and counter-financing of terrorism (AML/CFT) controls.

9. ESG and Financial Crime

The integration of Environmental, Social, and Governance (ESG) factors with financial crime compliance is accelerating. Organizations are recognizing that ESG-related misconduct often correlates with financial crimes, requiring enhanced due diligence approaches.

Key integration points include:

-

Supply chain risk assessment incorporating human rights and environmental factors

-

Enhanced screening for companies involved in illegal environmental practices

-

Corporate sustainability due diligence directives linking ESG compliance to financial crime prevention

Financial Crime Compliance Challenges

Following are the three major challenges banks and financial institutions encounter when it comes to meeting various financial crime compliances and regulatory requirements.

1. Rapidly Changing Regulations

Preparing for a rapidly changing regulatory environment is a challenge for the banking and finance industries. Failure to comply with federal laws and industry regulations can lead to reputational damage and incur legal penalties. Thus, banks and financial institutions need to be aware of the changes, understand the impact of the regulation, and implement the necessary changes to meet the regulatory changes.

2. Cyber Attacks

The financial services industry is one of the prime targets for cybercriminals. It includes financial crimes, such as stealing credit card or debit card information, gaining access to accounts to initiate unauthorized transactions, identity fraud, and so on.

Even though banks impose the strictest security policies, the risk of cyber security breaches and falling victim to attacks, such as ransomware, malware, phishing, and denial of service attacks, are quite high, which can lead to heavy costs and penalties. It can have dramatic consequences for both customers and financial institutions, irrespective of their size.

3. High Compliance Costs

Compliance costs increase with the increase in individuals or entities operating in different jurisdictions. The average cost to meet the various regulatory compliance, such as AML/CFT, is estimated to be ~$5.5 million. For non-compliance, it is ~$15 million.

Growing Need for Financial Crime Compliance

Financial crime and fraud is a trillion-dollar industry growing at a rapid scale with more sophisticated fraud techniques, such as Synthetic Fraud—also referred to as the crime of the new millennium.

According to one report by Thomas Reuters, the cost of organized financial crimes including human trafficking and slavery was estimated at a staggering $1.45 trillion in 2018. And almost 50% of large APAC organizations have been victims of financial crimes, such as money laundering and fraud.

In addition, companies including banks and other financial institutions spend 3.1%—an aggregate of $1.28 trillion—of total annual turnover to combat financial crimes.

Besides economic losses, financial crime also causes immeasurable harm to the world and humanity. The proceeds of financial crimes are generally used in the financing of terrorism, the proliferation of weapons of mass destruction, human rights abuses, and environmental crimes.

Financial Crime Mitigation

Financial crime mitigation requires banks and other financial institutions to identify vulnerabilities and implement the controls and systems to prevent financial crimes. To achieve this, they can put the following controls in place:

- Batch-level real-time transaction and behavioral monitoring for fraudulent transactions or activities, including suspected money laundering activities

- Real-time global watchlist screening and PEP matching

- KYC risk profiling, Customer Due Diligence (CDD), and Enhanced Due Diligence (EDD)

Banks and financial institutions can also follow the top five key strategies to enhance the efficiency of financial crime compliance programs.

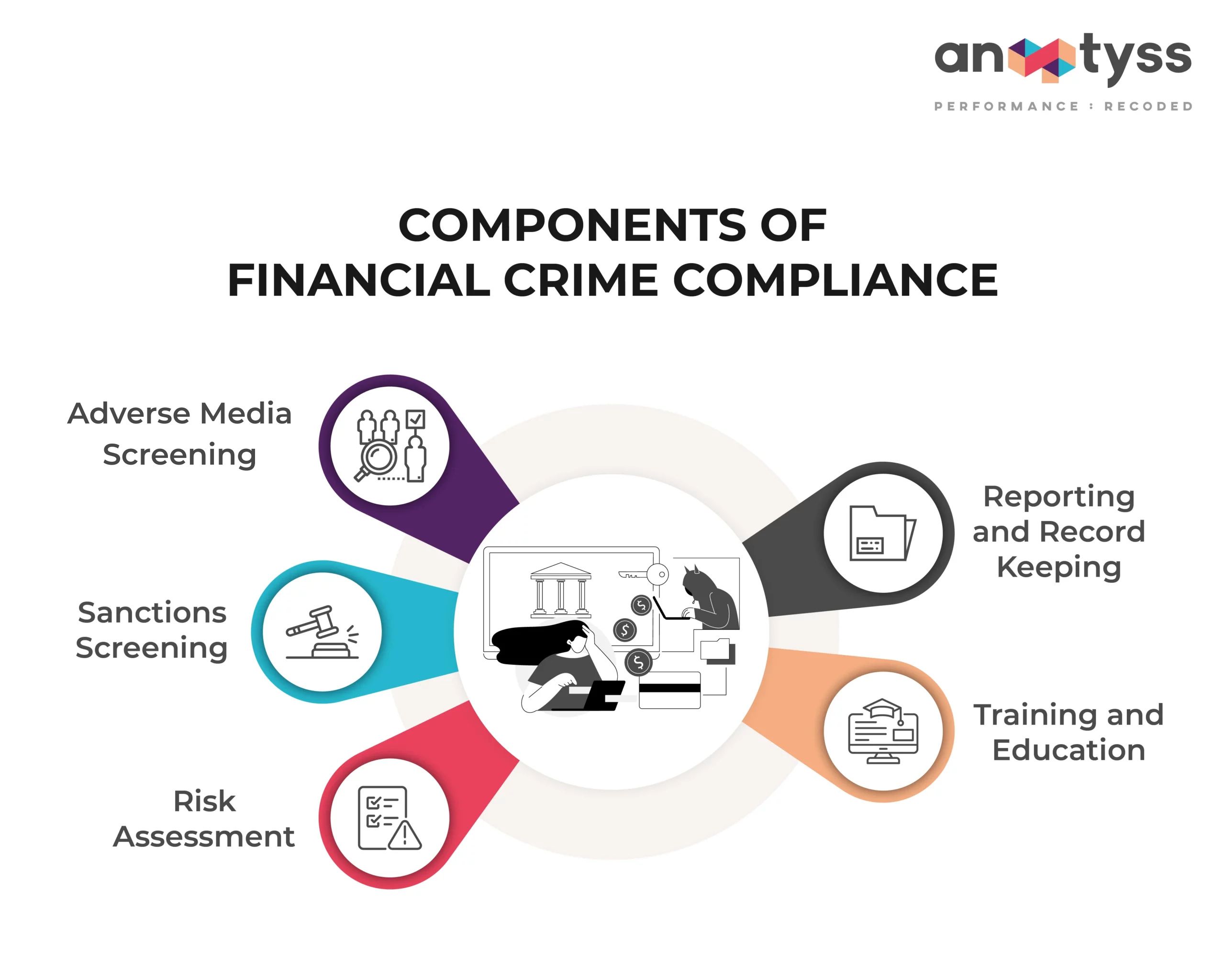

Components of Financial Crime Compliance

Financial crime compliance encompasses several key components:

1. Adverse Media Screening

Adverse media screening or negative new screening (media monitoring) is one of the KYC processes that comes under the CDD umbrella. It helps identify and analyze damaging information about a person, organization, or entity from different online and offline media channels, including social media.

2. Sanctions Screening

Financial institutions must screen transactions and customers against international sanctions lists or collected customer data for effective financial crime compliance (FCC). It helps financial institutions detect sanctioned individuals, entities, or countries before conducting any business or transaction with them.

3. Risk Assessment

Banks and other financial institutions must conduct periodic risk assessments to identify potential hazards, and weaknesses, and analyze the effects before they occur. This helps them effectively adapt their compliance strategies accordingly.

4. Reporting and Record Keeping

Financial institutions must maintain accurate and accessible records and report certain transactions and suspicious activities (SAR) to regulatory authorities. This is a critical step to demonstrate control over the customer onboarding process. These records also help in investigating the audit trail of any money laundering or terrorist financing activity.

5. Training and Education

Staff members need to be adequately trained to recognize and address financial crime risks effectively. Fostering a deep understanding of financial crime risks and compliance requirements helps create awareness about the intricacies of various financial crimes and empowers individuals within banks and financial institutions to navigate a complex regulatory landscape. It helps employees:

- Stay updated, and adapt to emerging threats

- Detect suspicious activities

- Assess risks

- Develop robust compliance frameworks

- Enhance skills for more effective detection and prevention of financial crimes.

6. Ongoing Monitoring

Perpetual KYC processes are becoming standard, with dynamic risk scoring and integration of third-party data sources.

7. Audit & Program Reviews (NEW)

Routine independent reviews are critical to identify gaps and foster continuous improvement in FCC programs.

Financial Crime Compliance Solutions: Manual Vs. Digital

Digital financial crime compliance solutions, such as Robotic Process Automation (RPA) embedded with artificial intelligence and machine-learning capabilities, can help address the challenges in traditional solutions with real-time tracking and monitoring of transactions with high accuracy.

By leveraging these intelligent digital solutions, banks, and financial institutions can analyze the data and detect suspicious activities and transactions. They can also generate audit trails to support compliance and save the organization from penalties and the high cost involved in the manual or traditional approach, which is prone to errors.

Technology in Compliance

The year 2025 marks the year when AI transitioned from experimental to essential in financial crime compliance. Financial institutions are experiencing dramatic improvements in detection capabilities, with AI-driven systems reducing false positives by up to 45% and achieving operational savings of 50% or more through automated data aggregation and case narrative creation.

The RegTech market is projected to exceed $22 billion by mid-2025, growing at a CAGR of 23.5%. This expansion reflects increasing investment in technology solutions that address compliance challenges while improving operational efficiency. Future technological developments include:

-

Generative AI applications for compliance documentation and reporting

-

Quantum computing implications for encryption and data security

-

Advanced analytics platforms providing real-time risk intelligence

-

Cloud-native solutions offering scalability and flexibility

Proven Solutions in Action: FCC Success Case Highlights

The journey from regulatory compliance to real-world impact is best illustrated through tangible results. The following table highlights a selection of our most impactful Financial Crime Compliance (FCC) success stories, showcasing how targeted solutions have delivered measurable improvements for leading banks and financial institutions in the United States.

| Case Study & Link | Description | Key Value |

|---|---|---|

| Consultative BSA/AML Risk Mitigation for US Community Bank | Implementation of a BSA/AML-focused program for regulatory risk reduction and compliance with FDIC directives. | Regulatory risk mitigation, compliance enhancement |

| Automated Data Validation & Accurate Fraud Detection | Deployment of an automated data validation tool that improved fraud detection accuracy by 48%. | Fraud detection, operational efficiency |

| 45% Reduction in Operating Costs for Regional Community Bank | Process reengineering and automation leading to significant cost savings and sustained regulatory compliance. | Cost reduction, process automation |

| 75% Reduction in AML False Alerts (ALFA Solution) | Introduction of ALFA, an AI/ML-based system that streamlined sanctions screening by reducing false positives. | Sanctions compliance, accuracy improvement |

| Flagged 100% Fraudulent Transactions with ML | Enhanced fraud detection system using machine learning algorithms to identify all fraudulent transactions in the test period. | ML-driven fraud prevention, compliance support |

Strategic Recommendations for Banks and Financial institutions

Immediate Priorities (2025)

Focus on rapid implementation of technology-driven solutions to address current regulatory and operational challenges.

-

Implement AI-enhanced transaction monitoring systems – Leverage artificial intelligence to minimize false positives and improve real-time anomaly detection.

-

Upgrade KYC processes – Automate identity verification and enable continuous monitoring to stay ahead of financial crime.

-

Enhance sanctions screening frameworks – Adapt systems to handle dynamic sanctions lists and ensure instant alerts for red flags.

-

Integrate ESG considerations – Align risk assessments with environmental, social, and governance risks for a sustainable compliance approach.

Medium-term Objectives (2026)

Build integrated compliance and risk infrastructures that are sustainable, scalable, and data-driven.

-

Develop comprehensive digital asset compliance programs – Prepare for increasing crypto oversight with robust policies and reporting tools.

-

Establish cross-functional teams – Break down silos by uniting compliance, technology, and operations under shared goals.

-

Implement advanced analytics platforms – Use data science to anticipate risks and make proactive compliance decisions.

-

Strengthen third-party risk management – Increase visibility into supply chains and ownership structures to reduce exposure.

Long-term Vision (Beyond 2026)

Create a resilient, adaptive, and proactive compliance ecosystem that evolves with global regulatory landscapes.

-

Build adaptive compliance frameworks – Design systems capable of scaling with new threats, laws, and technologies.

-

Develop industry collaboration mechanisms – Foster partnerships to share intelligence and raise sector-wide defense standards.

-

Integrate compliance by design – Embed regulatory requirements throughout the organization’s processes and systems from the ground up.

-

Establish comprehensive risk culture – Promote a consistent tone at all levels, ensuring everyone owns and understands compliance responsibilities.

Consultative Approach for Financial Crime Compliance Management

Financial crimes, such as money laundering, terrorist financing, fraud, bribery, and corruption, pose a greater threat to the integrity of banks and financial institutions across the globe. Failure to manage the risk of financial crime can have severe consequences, including loss of reputation and goodwill, penalties, and regulatory sanctions.

At Anaptyss, we help banks and financial institutions fulfill their financial crime compliance obligations in a customized manner with our Digital Knowledge OperationsTM (DKOTM) framework. The DKOTM framework empowers banks of any size to protect their customers, and reputation and avoid regulatory fines or sanctions.

Interested in knowing how the DKOTM-based solution approach can help your financial institution to attain financial crime compliance? Read how Anaptyss offered a consultative BSA/AML-focused risk mitigation program for a US-based community bank by implementing the DKOTM framework to meet the regulatory requirements.

Write to us: info@anaptyss.com.